Key points of the BVG reform

To be put to the vote on September 22 following a referendum, the occupational pension reform aims to strengthen the financing of the 2nd pillar, maintain overall pensions and improve coverage for part-time workers. Laudable objectives, to be sure, but are the means proposed to achieve them the right ones? That’s the question. Here is a summary of the reform points and the opinion of one of our BVG experts.

- What are occupational benefits?

- What changes does the reform propose?

- Our expert’s opinion

- Further information

How the 2nd pillar works can be a complex subject for anyone who is not an expert in the field. Reforming this mechanism is equally complex. That’s why we’ve prepared a summary of the proposed changes, which we hope will help you see things more clearly in the run-up to the vote.

What are occupational benefits?

For many people, occupational pension provision, or the 2nd pillar, is an important complement to the AHV (1st pillar). In theory, the 1st pillar is designed to cover the basic needs of the population, while the 2nd should enable people to maintain their usual standard of living. During their working lives, employees and their employers contribute to their Pension fund to build up a retirement capital that will be used to pay their pensions in the future. Up to a certain income, the law sets minimum requirements in terms of retirement contributions and benefits. The aim of the reform is to adapt some of these minimum requirements to today’s changing world.

What changes does the reform propose?

So what does the 2nd pillar reform, which will be put to the vote at the end of September, aim to change?

1. A change in pension contributions

The minimum amount that must be saved each month in the 2nd pillar depends not only on salary level, but also on the age of the insured person.

Contributions paid by workers and employers increase with age: employee contributions paid for older workers are higher than those paid for younger ones, which can put older people at a disadvantage in the job market.

As Pittet Associés explains, “the current four levels of bonuses (7% for 25-34 year-olds, 10% for 35-44 year-olds, 15% for 45-54 year-olds and 18% for 55-65 year-olds) would be replaced by two levels (9% for 25-44 year-olds and 14% for 45-65 year-olds). This measure is designed to encourage the recruitment of people over 55, by eliminating the additional cost associated with their high contributions”, but also enables young people to save more and faster, to benefit from the interest paid on their retirement capital.

2. Adjustment of the insured or contributory salary

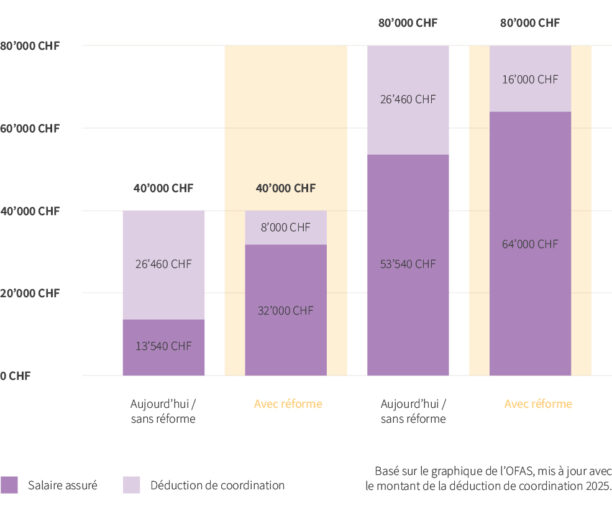

In the 2nd pillar, not all salary is insured: a certain amount is deducted, known as the coordination deduction. This amount is currently CHF 25,725 (CHF 26,460 from January 1, 2025), irrespective of salary and degree of employment. This coordination deduction affects low-income workers the most. Under the reform, the deduction will no longer be a fixed amount, but will amount to 20% of salary. Salaries will therefore be insured up to 80%. This means that, particularly for low-income earners, a significantly higher proportion of salary will be insured, which in turn means that future pensions will generally be significantly higher.

As Pittet Associés notes, “The adjustment of this deduction should make it possible to take into account an insured person’s degree of employment, which is not currently provided for in the LPP. This would enable people working part-time to cover a larger proportion of their salary under the occupational pension scheme.”

The deduction currently consists of a fixed amount of CHF 26,460 (figure 2025). If the reform is approved, it will rise to 20% of gross salary. The infographic above shows two calculation examples: for members of pension funds offering only the legal minimum, the insured salary corresponds to around 36% of a gross salary of CHF 40,000, compared with around 68% of a gross salary of CHF 80,000; if the reform is approved, this percentage will rise to 80% in both cases (Source OFAS). .

3. Lowering the threshold for access to occupational pension plans

As Pittet Associés explains, this threshold represents the minimum annual salary that an employee must receive from a single employer in order to be insured under the occupational benefits scheme. Currently set at CHF 22,050 (CHF 22,680 from January 1, 2025), it should be lowered to CHF 19,845 (CHF 20,412 if the reform were to come into force on January 1, 2025, but this will not be the case, as the reform will come into force in 2026 at the earliest). This reduction in the access threshold should make it possible to cover a greater number of employees under the occupational benefits scheme, particularly those on lower salaries, working for several employers or certain part-time workers. According to the Raiffeisen Pension Barometer 2023, around 70,000 people would be newly insured with the lower entry threshold.”

4. Reducing the conversion rate

Let’s start by reminding you what a conversion rate is: it’s the rate that converts the capital acquired into a pension at the reference retirement age. It therefore determines the amount of the future annual pension received during retirement. The reform proposes lowering this rate from 6.8% to 6.0% for the compulsory part of occupational benefit plans. At this rate, for retirement savings of CHF 100,000, the annual pension would currently be CHF 6,800, compared with CHF 6,000 if the reform were adopted. However, together with the other measures described above, the aim of the reform is to achieve a higher level of accumulated assets at retirement, with no reduction in pension. This is correct for a full career in the new system. For those already working and close to retirement, the reform provides for compensatory measures for those retiring within 15 years of the reform coming into force.

5. A pension supplement for the transitional generation

The main compensatory measure is a pension supplement for the transitional generation (15 years after the reform takes effect). For people retiring within 15 years of the reform coming into force, the increase in retirement assets will not be able to compensate for the drop in the conversion rate before they have retired.

This is why the reform provides for a pension supplement calculated on the basis of year of birth and accumulated retirement savings at the time of retirement. It will amount to a maximum of CHF 200 per month and will be paid for life. It will be financed by the Pension funds and by employee contributions from all employees and employers.

Our expert’s opinion

As you can see, the subject is complex. So we asked our pension expert, Sébastien Barbey, Head of Pension Fund at Loyco, what he thought of the reform.

“For my part, I’m rather in favor of this reform, as it allows us to adapt the minimum parameters to be respected for occupational benefits to the evolution of society. That’s right:

- Lowering the affiliation threshold means more workers can benefit from the 2nd pillar.

- The coordination deduction as a percentage of income (instead of a fixed amount) avoids disadvantaging part-timers.

- Lastly, the adjustment of pension contribution rates to 2 levels instead of the current 4 avoids potential discrimination in hiring older workers.

Admittedly, the BVG remains a costly system for low incomes and modest accumulated amounts, due to asset management fees, but it is a highly complementary system to the 1st pillar. Together, they enable us to cope with the various changes in our society, such as an ageing population and fluctuating financial markets. In my opinion, the transitional measures are the downside of this reform. Starting out with a good intention to partially compensate for the reduction in the conversion rate from 6.8% to 6% as soon as the reform comes into force, they appear to be very complicated to implement, but certainly remain the least costly solution for achieving the objective. All in all, I remain in favor of the overall package, with 15 years of complicated transition for what I believe will be a positive result in the long term.”

If you still can’t make up your own mind, you can still consult the many sources of information on the subject, a small selection of which you’ll find below.

Further information

- Reform of the occupational pension plan (BVG) – admin.ch

- The challenges of BVG reform – Pittet Associés

- BVG reform – September 22, 2024 – Votations – easyvote.ch

- BVG reform: What’s it all about?

- BVG 2024 reform: what’s it all about?